What happen to the wealth creation?

Why it shouldn't surprise anyone that a 3rd of Americans who make over $250,000 a year are broke.

I can’t help but feel a bit of deja vu as I write this newsletter. Indications of economic instability, rising consumer debt, contractions in the public and private equity markets, layoffs en-mass at tech companies small and large and…the icing on the cake? The affirmation of a society addicted to easy money:

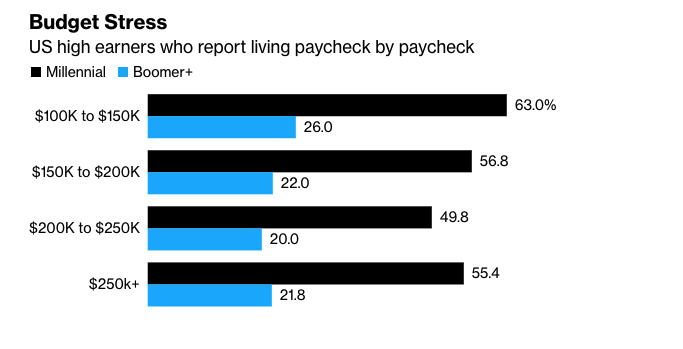

1/3 of Americans who make over $250,000 are living paycheck to paycheck.

The insanity continues when we realize that over 55% of millennials (probably the people reading this newsletter) who make over $250,000 are living paycheck to paycheck!

I can’t help but think how problematic this is in a good economy, but I genuinely fear for anyone experiencing this level of financial hardship as we approach a season of uncertainty. It is easy to mask bad decision-making during extended periods of growth; sometimes we achieve success in spite of our actions, not because of them.

In 2018, I first started documenting my journey of paying off $170,000 of student loan debt (ps — mission accomplished) but along the way, I wrote many articles targeted toward high-income earners (loosely defined as people who make over $100,000/annually) on how to write a personal budget. Guys and gals, this is step zero. If you’re encountering financial stress, maybe you have more months at the end of your money, or you just don’t know where to start: please read these guides! Originally posted on medium way back in 2018, they’re just as relevant in 2022! Get on a budget immediately!

Please consider reading the book I published in 2020: “Educated but broke — You are too smart to be this broke”. If you can’t afford it, message me and I will give you a free copy.

But alas, how did this happen? How is it possible that a 3rd of our highest income earners live paycheck to paycheck? I am certain the answer is access to cheap debt and an unwillingness to save. US households in aggregate have $16 trillion of outstanding consumer debt. That is a 16 with 12 zeros behind it or: $16,000,000,000,000.

The outstanding balance is $1.7 trillion dollars higher than before the end of 2019, before COVID-19. In the first quarter of 2022 our nation collectively added $266 billion of new debt to the balance sheet, and our savings rate is at a record 50 year low.

This is what happens when we embrace the ‘cheap money’ philosophy. You’ve heard it plenty of times:

“money is so cheap, we can borrow at 3% and invest at 8%” or

“I can take out a line of credit from my house and buy an investment property, then have the renters cover the mortgage” or

“the government is going to forgive my student loans, so there’s no point in paying it off” or

“smart money takes loans against their equity rather than liquidating their assets, this avoids a taxable event” or

“Don’t let your money just sit in your savings account, make it work for you!” (this one is my personal favorite)

It goes on and on. These are quotes I’ve heard so many times, from so many different people, who are successful and smart. They are all wrong. Look at the performance of the market YTD month ending November 2021 vs May 2022. SP500 up 26% vs down 13%

People who were investing in the 2021 euphoria are now in a world of hurt. I was having lunch with a friend earlier this week, his company IPOed in November 2021 but was unable to liquidate his holdings due to his lock-up window. His net- worth has decreased by 50% in 2022 YTD. He’s lost millions of dollars over the past 6 months. Ouch.

We’re not immune from this downturn, even in one of my brokerage accounts where I manage a ~ $300,000 portfolio based on an 80/20 split of index funds vs individual stocks, the past year has been less than pleasant. I would have faired better just letting the money sit in my savings account. Maybe the bogleheads were right?

Moreover, housing has reached record levels of unaffordability. The home price to median income ratio, a measure of how many years of gross income a house costs, is now approaching 8x. This is the highest in the history of housing, ever. The housing bubble in 2008 had a 7x multiple.

Irrational expectations drive irresponsible lending which inflates everything from stocks to houses; until it all crashes and burns. We’re seeing this in public and private equity valuations now. The value venture details declined 22% y/o/y in the US, and 44% in China. Housing prices will follow Q42022, I am convinced.

Rates are rising, money is no longer free, and that has massive implications for valuations and fundraising,” it said in a presentation for its portfolio companies. — Sequoia Capital

Our friends at the Goldman Sachs & Company, have pegged a US recession within the next 24 months at 35%, citing a competitive labor market with 5.3 million vacant jobs. GS is betting that Biden’s immigration policy will solve the worker shortage. I’m personally holding my breath until we get past the mid-term elections, it’s not looking good for the Democrats.

My advice to everyone reading this is to prepare for a cold winter, especially if you work in the tech space. Tesla is firing 10% of its workforce, Carvana just fired 2,500 employees, Coinbase is rescinding job offers:

Watch the SP500, if it dips below 3900 again, I will be aggressively buying. This is your upside. Continue to max out your retirement accounts and prepare for a season of uncertainty. My wife and I making sure we have 18 to 24 months of expenses, just in case. Stay safe.

John Cook

San Francisco, CA

June 5th, 2022

www.frontruncrypto.com

Improve your knowledge by reading these articles:

There’s quite a bit of uncertainty as to whether or not the market has bottomed out or if there’s more to come. The team at LPL put together a fantastic study comparing the YTD performance of the SP500 during midterm election cycles, lots of upside once we’ve hit the bottom! The conclusion:

Looking at all the midterm years going back to 1950, only two have seen their yearly low before May 19, when the S&P 500 made its closing low two weeks ago. We would note though, that the depth of this correction is almost exactly in line with the average mid-term year pullback. And regardless of when we make that bottom, as the chart below shows, the gains a year after the low have been substantial with a more than 30% average return and only one occurrence falling short of a double digit gain.

China’s Gen-Z brands have the power to make or break Western Brands

In what I hope to be the capitulation of US brands bowing to the Chinese communist party; Gen-Z Chinese have made a big, bold statement: They’ve got money to burn, eschew foreign labels, and are driven by a swelling sense of nationalism that can ensnare even the biggest global brands. American brands are losing their allure in the Chinese market as its citizens opt for Chinese-made products. Maybe it’s time for the US consumer (and brands) to start cheering for the home team.

Sarah Lin, a 22-year-old student in Beijing, said her parents still get excited by items that only have foreign-language labels because they assume it’s a premium product. But during the time she studied abroad, she realized many brands considered high end in China are mass-market names at home. Now, she prefers to research products and is happy to buy domestic names due to their improving quality and designs that appeal to her.

Hindenburg Research never fails to deliver, named after 1937 Hindenburg blimp disaster; the team identifies mispriced assets, writes compelling cases against its current valuation, then shorts the position. Earlier this month they called twitter’s go-private price of $54.20 to be overvalued, implying a target price of $31.40, citing Musks’ power position in the transaction:

As a result of these developments, we believe that if Elon Musk’s bid for Twitter disappeared tomorrow, Twitter’s equity would fall by 50% from current levels. Consequently, we see a significant risk that the deal gets repriced lower.

Quote of the week:

“It amazes me how people are often more willing to act based on little or no data than to use data that is a challenge to assemble.” — Robert Shiller