Real world asset on-chain tokenization & risks

A review of real-world assets, collateral methods used to fund off-chain investments and its associated risks

Dear frontrunners,

There has been a re-emergence of the “real world asset” (RWA) narrative within the crypto ecosystem: On-chain loans used to fund off-chain investments.

Off-chain investments mean deploying capital to purchase risk-free assets like US Treasury Bonds, finance accounts receivable loans, fund real estate investment projects, or even invest in unsecured debt used to finance smartphone purchases for consumers in 3rd world countries. My suspicion is the renewed interest was fueled by last month’s launch of rwa.xyz: analytics on real-world assets.

In this analysis, we’ll review the three primary methods for collateralizing loans on the blockchain and its associated risks.

On-chain collateral

On-chain collateral means the collateralized asset is locked on the blockchain via a smart contract. An example is the Maker’s stablecoin Dai. At its core, Maker uses eth as on-chain collateral to create the Dai token pegged to the value of 1 US dollar (USD).

Since there is no native USD-native token on Ethereum (stablecoins like USDC are fiat collateralized off-chain, and Terra/Luna was a bust) DAI must be backed by another asset, usually, but not always, Ethereum. When DAI is minted, the borrower must first lock enough ETH as underlying collateral in a smart contract provided by Maker. Since the USD/ETH exchange rate is not fixed, this requires over-collateralization. If the value of the underlying ETH falls below the minimum threshold of the outstanding Dai value, the smart contract will auction off the collateral to close the debt position in Dai.

Another example is Aave, a pool-based lending protocol for earning interest on deposits and borrowing tokens against said deposits. Anyone can borrow from the pool by depositing collateral such as ETH or WBTC. The corresponding borrower interest & depositor yield are determined algorithmically. Each asset in the pool has its own loan-to-value parameter, which dictates the on-chain collateral ratio. If a position is undercollateralized it is programmatically liquidated and its on-chain assets are auctioned.

Below is a sample picture of Aave’s lending UI with ~ $300 of WBTC/ETH collateralized to borrow $150 ETH.

Again assets are over-collateralized, on-chain & subject to automatic liquidation. A simplified mental model is: if (borrowed asset = ~85% deposit amount) THEN liquidate.

Example 1:

I deposit $1000 ETH to borrow $500 BTC

My value of BTC moons to $850 while ETH stays at $1000

Result = automatic liquidation

Example 2:

I deposit $1000 ETH to borrow $500 BTC

My value of ETH decreases to ~ $588 while BTC stays at $500

Result = automatic liquidation

For more information consider reading Maker's white paper and Aave’s risk parameters.

No collateral

In a no-collateral defi loan, the promise is entirely trust-based. Altruistic no-collateral investments include Alma’s Almavest Basket 3 which provides uncollateralized consumer & personal loans to individuals and small businesses in India via Goldfinch’s “borrower pools”, depicted below:

Liquidity providers (crypto folks) deploy capital (stablecoins) to a borrow pool/ lending pool/lending vault (they all mean the same thing).

Off-chain lenders draw/replenish capital from said borrow pool after an assessment of the lender’s on-chain/off-chain creditworthiness via a “team of experts” 🙄

Off-chain lenders act as loan originators to far-away borrowers who pretty please with sugar on top pinky-promise to pay back the off-chain lender who in turn repays the Goldfinch borrow pool which enables liquidity providers (crypto folks) to withdraw their deposit inclusive of new yield.

No-collateral on-chain loans are again risky because of counterparty failure. The “counterparty” for the liquidity provider is the lending business, and the counterparty to the lending business is the end borrowers.

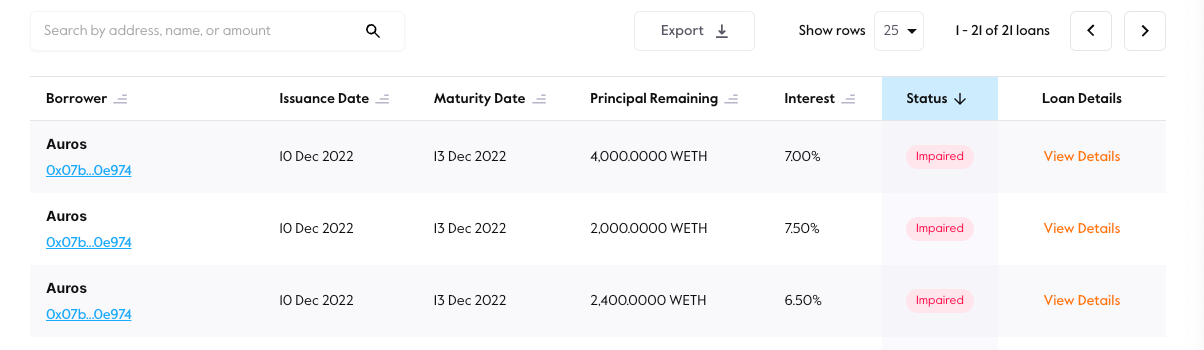

As we can surmise, with no collateral, “counterparty default risk” is at its highest. Especially when we consider prop trading firms who act as mercenaries with the singular goal of maximizing profits. For example, one month ago Maple Finance took an impairment loss on an 8,400 ETH loan by digital asset management firm M11 Credit.

Why? M11 acted as the portfolio manager of the 8,400 ETH pool and issued the entire amount to Alameda’s trading desk, who we now know was terrible at their job… and unfortunately for the liquidity pool providers, it was a no collateral loan.🪦

You see when big brain trading firms managed by finance professionals from Ivy League universities ask for a $30,000,000 eth-denominated loan using a presentation created by McKinsey…

…that outlines the deep institutional experience of the underwriting team…

..and the platform’s vision for sustainable yield with diversified exposure managed by a set-it-and-forget-it term sheet….

…there is no need for the inefficiencies associated with over-collateralized loans. Loan …collateralization is “not an efficient use of capital”. 🙄 Turns out that was a lie, and it is reflected in the token price of these firms. Maple Finance’s MPL token is down 95% y/o/y and Goldfinch GFI is down 96%.

Off-chain collateral

Off-chain collateral means the underlying assets used as collateral for an on-chain loan are managed with an escrow service, commercial bank, or trust “off of the blockchain”. A real-world asset like commercial real estate is an example of off-chain collateral. One such example that made me chuckle was Maker’s $24m DAI loan to finance the construction of 7 O’Reily Auto Parts & 3 Tesla collision and repair facilities:

There are many protocols facilitating on-chain borrowing collateralized with off-chain real-world assets & I encourage you to explore rwa.xyz when you have a moment.

You will see most RWA investment opportunities are on-chain loans enforced by smart contracts collateralized by off-chain assets to facilitate off-chain investment opportunities. From Goldfinch’s borrow documentation:

Borrowers collateralize their on-chain loan with off-chain collateral. Backers may require such an agreement to be in effect, either with them directly or with another Backer, in order to be willing to supply capital. In these cases, the legal agreement and potential Investor recourse are another important incentive for Borrowers. Currently, all loans on Goldfinch are fully collateralized with off-chain assets via this mechanism. - Goldfinch

This is a little wonky because if the collateral is securitized off-chain via escrow and/or a separate legal structure like a trust, the only component of the “loan” that is on-chain is the repayment mechanism in the smart contract.

Some platforms have got creative and minted NFTs that provide risk exposure & earn “yield” on the loan used to fund a real-world investment, but it’s really just an IOU. The $10m DAI loan funded by Maker was used to finance the construction of an O’Riley Auto Parts in the real world, not the meta! There is no on-chain mechanism with automatic liquidation because the collateralized asset does not exist on the blockchain.

Rather, in the event of a default, the agents of the borrower are “asked to liquidate the pledged collateral, convert it to USDC, and repay on-chain”:

… Borrower(s) are instructed to liquidate the pledged collateral, convert into USDC, and make payments on chain into the relevant Borrower pool. The Senior Pool and Backers are then able to claim their portion of the funds from the Borrower pool. - Goldfinch

Good luck. 🪦

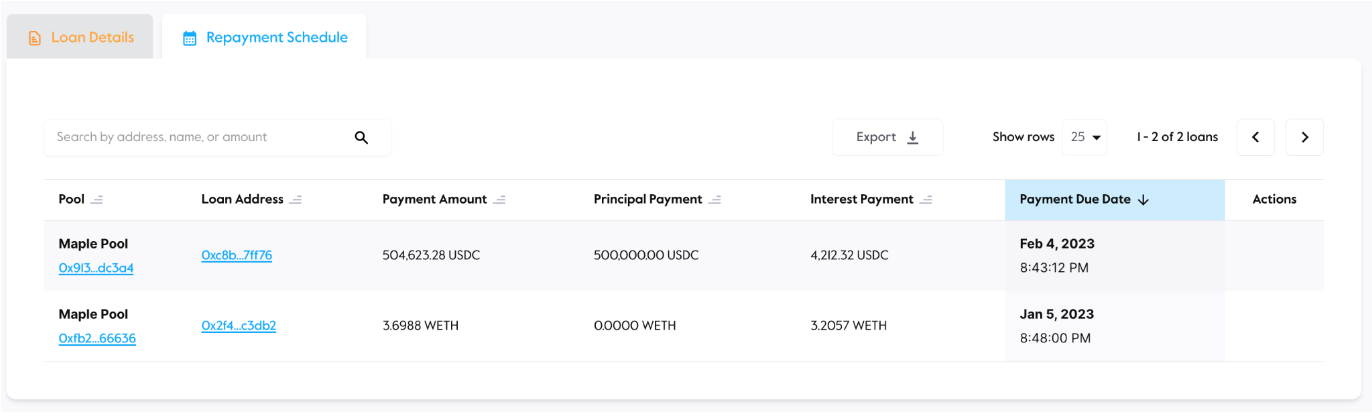

When you boil it all down, it’s just an escrow contract, a loan agreement, and UI on a web page where a borrower can go to “repay the loan” by sending USDC and/or ETH to a borrow pool wallet via a smart contract. Depicted below is Maple’s repayment UI.

Now that we’re all experts in efficient capital deployment & on-chain loan origination, set forth into the defi ecosystem, proceed with caution and be wary of capital-efficient and uncollateralized lending pools. For those interested in learning more, I recommend reading a white paper published by the Economic Research Division of the Federal Reserve Bank of St. Louis, titled “Decentralized Finance: On Blockchain- and Smart Contract-Based Financial Markets”.

To knowledge and wisdom,

John Cook

January 4th, 2023

San Francisco, CA

www.frontruncrypto.com

Article cover generated by DALL-E: “An abstract painting of Julius Caesar explaining on-chain smart contract loans to Alan Turing”