Mainstream mediocrity

How the talking heads on TV and their corporate investors chose to delete sections of their websites rather than report the truth on FTX.

Pro-tip: If you want to bring attention to yourself, start deleting sections of your website. Just follow the lead of Forbes, The Block, Digital Currency Group, and Sequoia Capital.

Dear frontrunners,

“The mainstream media coverage of FTX has been comprehensive and objective” - Said no one ever.

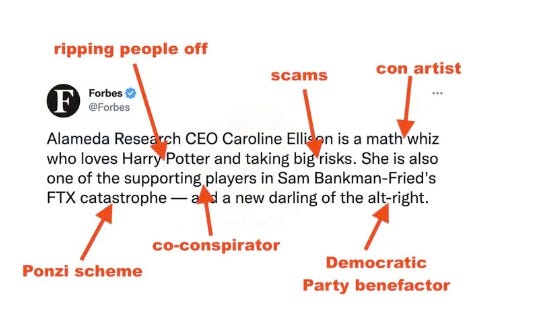

It should come as no surprise that the talking heads on TV and legacy print have failed to provide an accurate analysis of the FTX ponzi, government malfeasance, investor greed, the broader crypto collapse, and corresponding wealth destruction. Mainstream media (referenced as “MSM” throughout this analysis) has framed FTX, Alameda Research, and their executive team as:

Operators of a transparent exchange brought to its knees by a ruthless competitor - Forbes Digital

Victims of a Chinese corporate raider operating a questionable international crypto exchange - Financial Times

Complex, nerdy, and highly intelligent - The Block

Fortunately, this poor reporting is caught mostly via twitter, and these self-proclaimed “financial reporters” are forced to backtrack on their claims of “investigative journalism”. They mostly republish the article, without any footnote indicating an edit has been made post-publication… but the damage is done and the internet never forgets.

Smart money

Institutional investors and “smart money” venture capitalists are also guilty as charged. In an attempt to hide their participation in FTX grift, the organizations which made this scam possible are now re-writing their internet history by deleting entire articles and removing entire sections from their web page:

Digital Currency Group (DCG) completely removed its “Who we are” section which outlined its executive team, board members, and investors.

What would motivate a venture capital fund with $50 billion of assets under management to completely remove it’s about me section and go 100% anon? Aren’t website headshots the ultimate flex and humble brag?

DCG is the operator of the Grayscale Bitcoin Investment Trust (GBTC), a digital currency investment product, which is currently trading at a 45% discount relative to its underlying asset bitcoin.

This means that you can buy one dollar of Bitcoin for 55 cents (45% off). Sounds great right, why isn’t everyone loading into GBTC for an instant 85% return in the next bull market? The answer is Grayscale’s inability to provide any proof of reserves of its assets under management.

What makes this so damning is that Genesis Trading, a crypto trading desk owned by DCG (who again also owns Grayscale), just announced that their trading division has $175 million of exposure to FTX, its lending group has $2.8 billion worth of outstanding loans, and its investing platform has suspended customer withdrawals to “prevent a bank-run”.

I’m sure this has nothing to do with their overleveraged position, most likely on GBTC? DCG is the single largest holder of the GBTC asset, and GBTC was the preferred crypto investment vehicle during the last bull run. Trading desks like 3AC took investor deposits and entered into leveraged positions using GBTC. Since GBTC traded at a premium to its NAV, 3AC was able to post an instant profit as high as 38% back to its LPs, which fueled new investor deposits, which worked..until it didn’t.

There is now a growing concern that both Grayscale and Genesis Trading are illiquid and perhaps more interconnected than previously disclosed..but don’t worry, we have the investigative journalists and crypto enthusiasts at Coindesk to keep these bankers honest, right? Wrong. Coindesk is owned by Digital Currency Group. So much for objectivity.

Below, Coindesk discusses FTX’s exposure to USDT and its actual reserves, to which SBF literally responds:

“I’m not going to be able to prove to you, a 100%, exactly what’s there” - Sam Bankman-Fried

The lack of effort from Coindesk and their inability to hold SBF accountable is either a byproduct of incompetency or deceit. My unproven opinion is the symbiotic relationship Coindesk has with DCG and the broader crypto market via Genesis Trading is what perpetuates these soft-ball questions in what is clearly an attempt from SBF to side-step the tough questions.

But surely, the coastal elites in Silicon Valley, home of the microprocessor, Stanford University, and self-driving cars must be able to operate with a higher level of integrity than their crypto-degenerate counterparts. After all, Silicon Valley is at the forefront of new technology, helping founders and their companies change the world, it’s where one out of every 11,600 people is a billionaire, and one out of every 727 people is a multi-millionaire. These are the people we look to for guidance, right?

Wrong. BigVCCos fail all the time, in a speculator fashion but it is their hubris that prevents them from acknowledging any wrongdoing and instead attempts to re-write history by deleting their previous endorsement of FTX and SBF:

To quote the Sequoia capital article:

….I was talking to a future trillionaire. Whatever mojo he worked on the partners at Sequoia—who fell for him after one Zoom—had worked on me, too. For me, it was simply a gut feeling. I’ve been talking to founders and doing deep dives into technology companies for decades. It’s been my entire professional life as a writer. And because of that experience, there must be a pattern-matching algorithm churning away somewhere in my subconscious. I don’t know how I know, I just do. SBF is a winner.

If crypto publications like The Block aren’t able to report the truth

If the largest crypto publication in the world, CoinDesk, is beholden to the same forces responsible for the impending implosion of GBTC and Genesis

If the largest and most prestigious venture fund in the world won’t admit wrongdoing in its involvement with FTX

If the fintech and crypto desk of the Financial Times is unable or willing to call out the ponzi tokenomics of FTT and the FTX token

…how can we expect the media apparatus of the US government: CNN, Forbes, MSNBC, NYTimes, WSJ, Fox, etc to act with objectivity? The answer is we can’t.

NYTimes

The fintech and cryptocurrency desk of the New York Times published a “report” on the collapse of the FTX under the tutelage of megalomaniac SBF and concluded :

Around the time the crypto market crashed this spring, Ms. Ellison explained, lenders moved to recall those loans, the person familiar with the meeting said. But the funds that Alameda had spent were no longer easily available, so the company used FTX customer funds to make the payments.

According to a person familiar with FTX’s finances, the exchange lent as much as $10 billion to Alameda. - New York Times

How many times were the words “fraud”, “crime”, “illiquid”, “stolen”, criminal”, “back door”, or “hidden” used throughout the article? Zero.

How often did this “financial reporter” push SBF on the FTT token economics, FTX’s ability to control its total supply, or how FTX minted new money and used it as collateral for US dollar stablecoins? Not a single time..but hey, at least the guy wanted to make sure Sam was getting enough sleep in these tough times:

“You would’ve thought that I’d be getting no sleep right now, and instead I’m getting some,” he said. “It could be worse.” - Response from SBF on his sleep schedule

I’m sure it has nothing to do with SBF being an attendee at their upcoming “Business, Culture, and Politics Summit”. For gosh sake, it’s today’s most vital minds on a single stage! What blows my mind is how this summit is being advertised by a WSJ employee who is a self-proclaimed investigative journalist! Where is the investigation? We should not be surprised.

Wall Street Journal

My critique of mainstream media is their continued inability to report on facts that actually matter. In a complete puff piece authored by reporters within the finance bureau of WSJ, the article “How Caroline Ellison found herself at the center of the FTX Crypto Collapse” describes Caroline’s love for Harry Potter and Stuffed animals:

Caroline Ellison grew up in the Boston suburbs, the daughter of two MIT economists. At 5, she read the second “Harry Potter” book to herself, she said on the podcast. At 8, she wrote an analysis of stuffed-animal prices, according to Forbes. Her father, inspired by his daughters, wrote advanced-math textbooks for children bored by basic lessons.

…her vision for a socially impactful company…

She and Messrs. Bankman-Fried, Wang and Singh comprised the board of what they called the Future Fund, with the goal of making grants to nonprofits and investments in “socially impactful companies.”

…and how her rapid ascension to becoming the CEO of Alameda was accidental…

In a handful of podcasts and other public appearances, Ms. Ellison was quick to summarize her rapid ascent as almost accidental. She joined Wall Street straight from graduating Stanford University in 2016, though the move was less a calling than an answer to the question she found herself asking in college: What are math majors supposed to do with their lives, anyway?

How much time and content did WSJ dedicate to describing how Alameda Research used fake money created by FTX as collateral for US dollar-denominated stablecoins?

How much effort was put into to explaining the leveraged positions Alameda took on the FTX token collateralized loans, all of which ultimately went to zero

..or the overstatement of assets on their balance sheet…

…or the understatement of the real liabilities Alameda had exposure to via the co-mingling of depositor funds…

…or how institutional investors provided the capital which enabled Alameda to take these risks

..or how Alameda’s internal pitch decks included a 100% y/o/y return..

How much did time WSJ spend answering any of these questions with the pretense that Caroline Ellison was the CEO of Alameda when all of this happened? The answer, is, of course, zero. Throughout the analysis, she’s framed as a victim, an observer, in the FTX meltdown, and only makes reference to her pre-existing knowledge of the use of depositor funders as a backstop on Alameda’s liabilities in the very last sentence of the article. Good grief.

Forbes

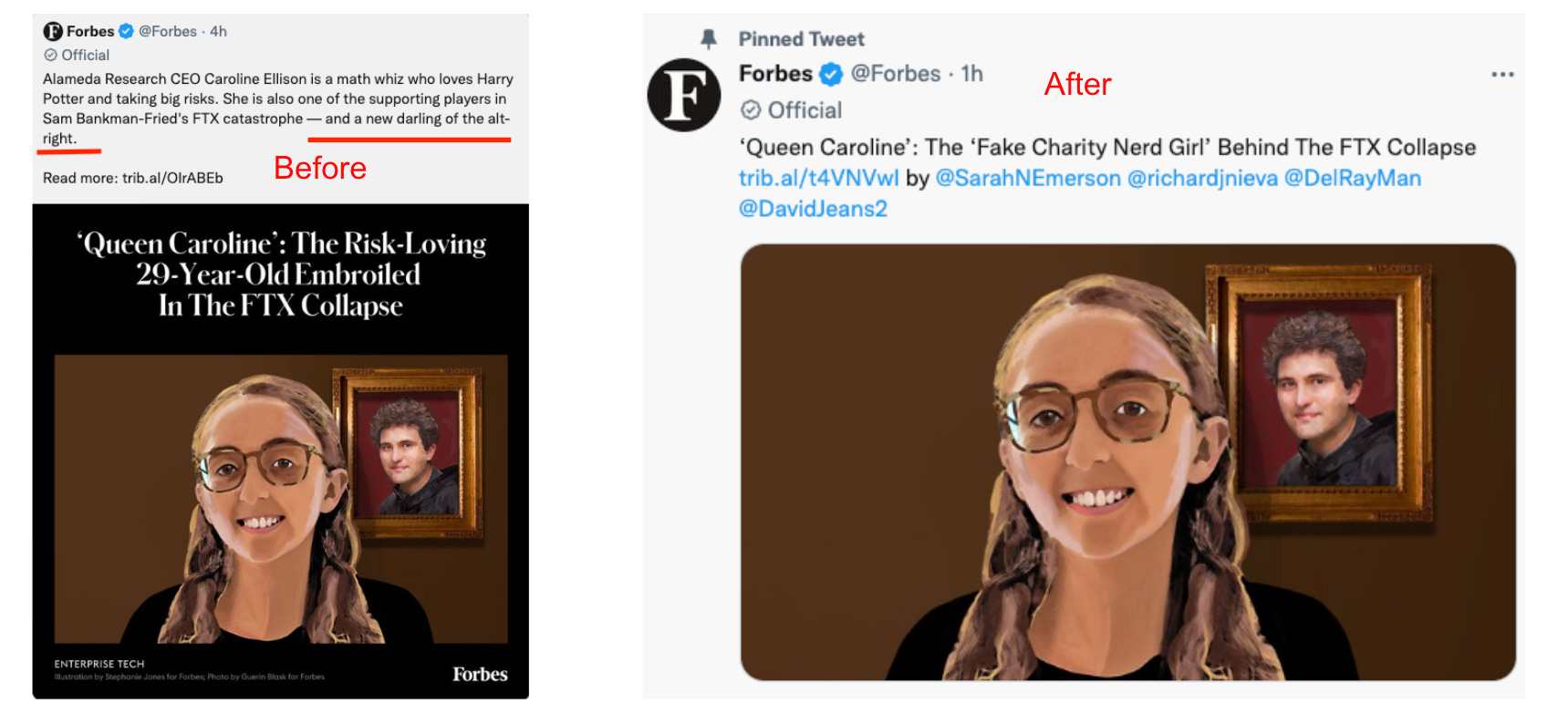

Even Forbes couldn’t resist politicizing the FTX meltdown as a byproduct of the alt-right, before getting downvoted into oblivion once the Twitterverse pointed out that FTX and SBF donated over $40 million dollars to the DNC in 2022. Can you believe Forbes sent an “investigative journalist” to the Bahamas for this garbage?

This is a more accurate representation of what the headline should say:

Surprised?

We should not be surprised. These MSM pundits are the same “experts” who portrayed SBF, the creator of a $28 billion Ponzi crypto coin, as the next Warren Buffet. The smartest people in the room told us that SBF’s quest for global domination was really just him earning to give. His vision of philanthropy where he helps as many people in the most efficient way possible is called effective altruism and should be the model for other executives and teams….

….It’s why FTX has a higher Leadership and Governance ESG score than Exxon Mobil….

…it’s also why SBF was on the cover of both Forbes and Fortune…

…these decisions are made same “experts” who heralded SBF and FTX as this generation’s “JP Morgan”…

…these are the same individuals who told us that SBF and FTX is “the white knight crypto” or “the Michael Jordan of crypto if you will”.

….these are the coastal elites distilling complex technology and business activity into digestible nuggets of wisdom for us plebians to understand, like how Sam Bankman Fried is the “patron saint of crypto”…

The problem is participation inequality

Mainstream media, its corporate investors, and the invisible handle of the billionaire class control the narrative and flow of information. This is called participation inequality. It is where one percent of the population generates 90% of the consumable information.

Information is disseminated from the one percent who act as the invisible hand controlling the flow of news; opaque or vague public policy, crypto scams, and financial analysis so complicated, it might as well be a foreign language. Social media serves as a tool to amplify the information created by the elite to serve their benefit, not yours. Special interest groups, corporations, technocrats, and legacy bankers all create narratives to expand their wealth and their knowledge, at your expense. Does this sound familiar? It is why we started Frontrun.

FTX is just the most recent example of this systematic flaw in America’s news and reporting apparatus.

This is the antithesis of open finance and a reminder to reject the status quo from all media organizations. Government oversight, a centralized body controlling the flow of information, and the creation of a “comprehensive regulatory framework” is not the answer to this round of wealth destruction, the FTX ponzi, or any 2nd and 3rd order effects of investor under-collateralized leveraged positions.

A decentralized, permissionless, financial system where contracts are enforced by code on an immutable ledger of transactions has not collapsed, nor has it experienced a bank run. Uniswap, Aave, Compound, Maker, et al, all continue to function as engineered. This is because counter-party risks are smart contracts, transactions are on-chain and liquidity is supplied by automated market makers. Bankruptcy is an impossibility on the blockchain. For those who need a refresher on why this is true, please review my previous article titled “There is no bankruptcy court on the blockchain”.

In a future analysis, we’ll cover why the mediocrity of mainstream media and smart money investors is really a function of a corrupt, mediocre, government bureaucracy that transcends both parties.

To knowledge and wisdom,

John Cook

San Francisco, CA

November 20th, 2022

www.frontruncrypto.com

Article cover generated by DALL-E: “An oil pastel painting of corrupt mainstream media reporters taking bribes from billionaires”

tweet of the week - “Pentagon, hexagon, octagon, mymoneygon”